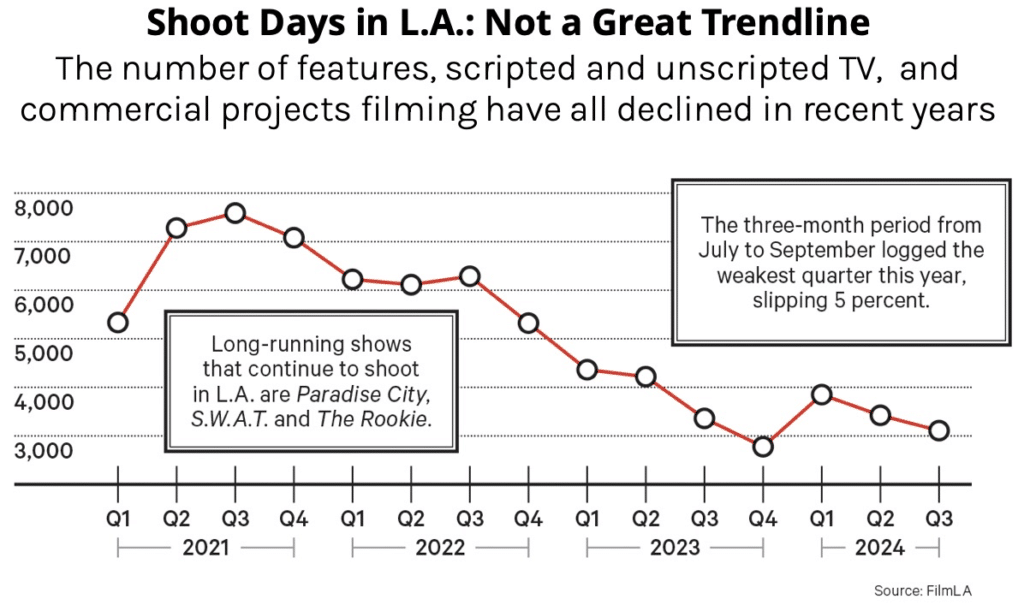

In the past 5 years Los Angeles investors and developers have pushed forward with both under-construction and planned developments of film studios and sound stages. It made some sense given the lack of vacancy in the booming streaming years. But since the SAG-AFTRA strike all bets are off for demand for film production. See above chart showing declining demand for film production of features and TV.

We could see some of the planned projects get shelved by cautious investors, or if they do build and demand doesn’t bounce back they could get burned. Only time will tell. And even if demand rebounds that doesn’t mean it will stay in LA as inter-state competition is hot along with Canada and other countries per the Hollywood Reporter article.