Bankruptcies in trucking are accelerating as tariffs, heavy debt, and post-pandemic overinvestment plague the industry. Some are warning recovery may be delayed until mid-2026.

The pandemic-era freight boom drew thousands of new entrants to the market, many of whom invested heavily in trucks and drivers based on unsustainably high spot rates. As freight demand cooled, those investments became a liability.

2025 was definitively worse than 2024. While 2024 showed some signs of market stabilization and even increased new freight carrier registrations, 2025 saw an acceleration of bankruptcies, record-breaking carrier exits, continued cost inflation, and persistent unprofitability. The hope that emerged in early 2024 was dashed in 2025 by factors including tariffs, tightened credit standards, and new regulatory burdens like stricter English proficiency requirements for drivers.

For industrial property, such as the IOS subcategory, the decline in demand for space from the trucking industry has led to a great change in the market. A few years ago available land was nearly impossible to find and now there are plenty of options to choose from in the Los Angeles area Metro. Land lease rates and sale prices have dipped considerably.

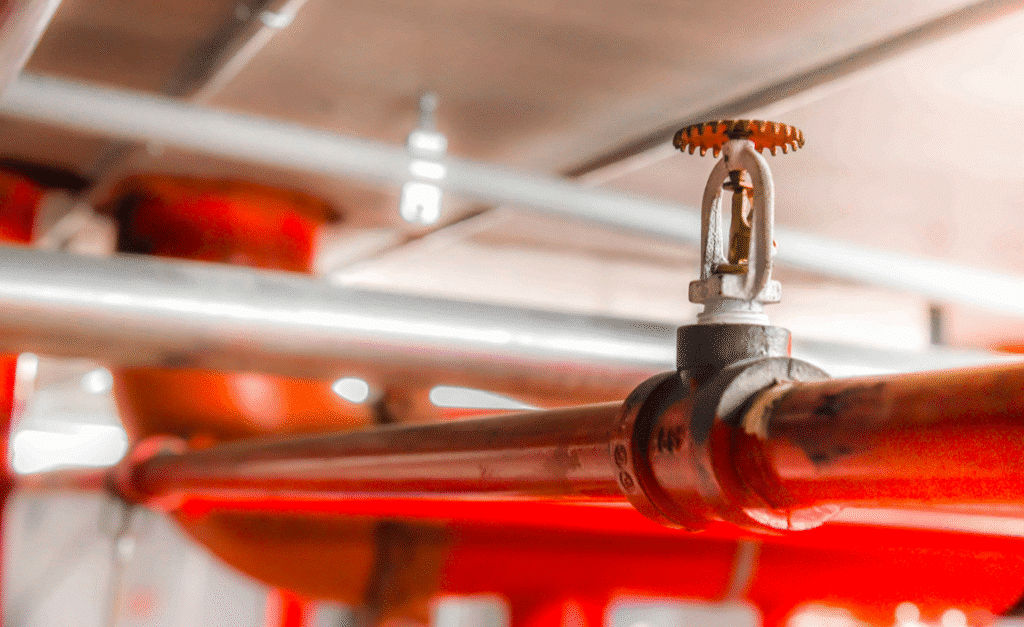

Fire sprinkler systems are highly effective fire protection measures that use water and pressure. Modern industrial manufacturing and warehouse buildings have these systems but many older buildings do not. The cost of fire insurance is often higher for buildings without sprinklers.

The 5 year system test and certification is typically paid for by the landlord but some industrial leases allow the landlord to pass this cost onto the tenant. Below are some of the key components that are tested:

Checking fire sprinkler heads (orientation, condition, and ability to transmit liquid).

Performing a forward flow test for backflow preventer.

Inspecting sprinkler control valves.

Inspecting sprinkler system alarm components.

Inspecting and testing low-pressure alarms.

Visibly inspecting pipes, gauges, hangers, drain valves, and all other relevant components.

Example 5 year certification sticker on fire sprinkler riser.

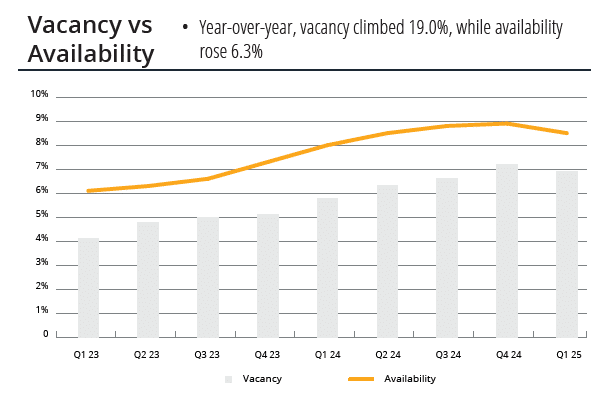

As the Vacancy Rate has climbed in recent years, more and more industrial warehouses are available and competing for buyers and tenants in the Central Los Angeles and Southern California market. Feel free to browse the below list of available warehouses that are greater than 100,000 square feet.

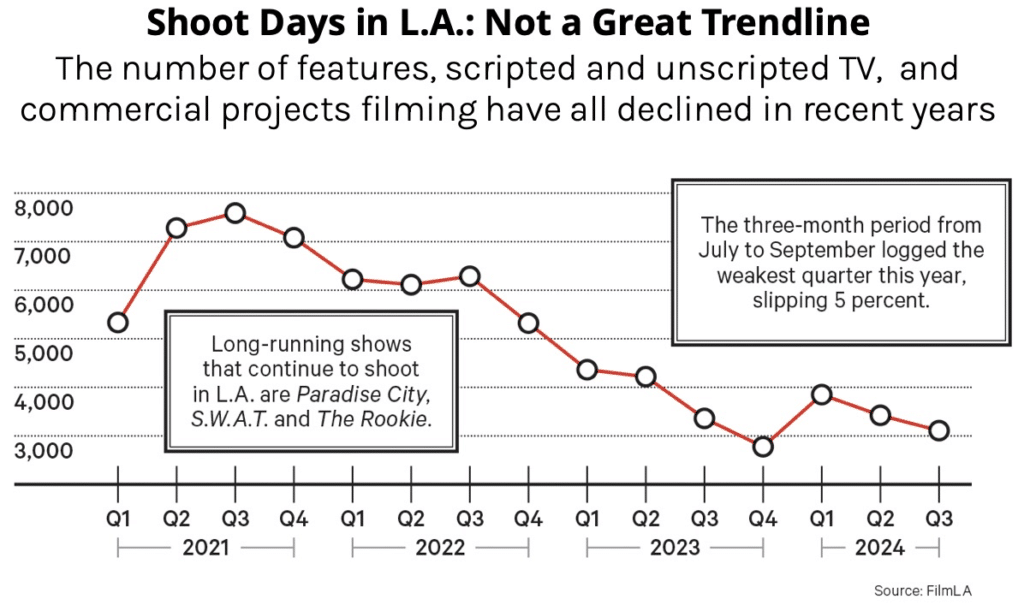

In the past 5 years Los Angeles investors and developers have pushed forward with both under-construction and planned developments of film studios and sound stages. It made some sense given the lack of vacancy in the booming streaming years. But since the SAG-AFTRA strike all bets are off for demand for film production. See above chart showing declining demand for film production of features and TV.

We could see some of the planned projects get shelved by cautious investors, or if they do build and demand doesn’t bounce back they could get burned. Only time will tell. And even if demand rebounds that doesn’t mean it will stay in LA as inter-state competition is hot along with Canada and other countries per the Hollywood Reporter article.

As with any insurance market, the commercial property insurance market is constantly evolving, with new trends and challenges emerging that can impact both insurers and policyholders alike. Across the country, there have been several regulatory changes in recent years that have added costs and increased compliance requirements for insurers in this space. Specifically in California, there has been an increase in non-renewal notices as many insurance companies withdraw from the marketplace, most notably in Los Angeles County but also throughout the entire state.

Premium Change for Commercial Property, Q1 2017 – Q4 2023 from The Council of Insurance Agents & Brokers.

California has become one of the most difficult places to write insurance, so many carriers are exiting the market, reducing capacity, or only looking to insure best-in-class buildings.

Risk. Concern has grown over the incidence of natural disasters including wildfires, flooding, landslides, and earthquakes. This has caused premiums to further increase and caused reinsurance costs to be passed down to policy holders.

Insurers also consider a property’s likelihood for litigation and heightened number of claims. Multi-family is considered high risk because the human factor by nature yields an increased frequency of claims. The same can be said of retail shopping centers where there is increased foot traffic. In essence, the more people, the more claims. Industrial buildings and office properties, on the other hand, are considered moderate to lower risk, unless they have a very high vacancy rate which can make them susceptible to theft.

Building Age: In Los Angeles where the building stock is aging, the preferred market prioritizes either structures built within the last 30 years or those with records reflecting regular maintenance and upgrades. Insurance companies don’t inspect properties every year, which can have unfavorable outcomes for buildings that go several years without review. For example, many carriers are shying away from Los Angeles’ Downtown and Garment District because of the high incidence of claims coming from older warehouse and manufacturing buildings that haven’t been kept up. A lot of these older buildings are being placed on the Excess and Surplus Market (E&S) when the risk is too high to insure, which results in higher rates, and in some cases, limited coverage.

Here are some strategies:

Maintain accurate records. Well-kept documentation is the best tool an owner can have to prove the maintenance and renovation of their property. Remember: to secure a carrier in the preferred insurance market, the building does not have to be new, but the systems must be up to date. A 100-year-old building can get placement if inspections and records reflect optimal maintenance.

Check your online presence. These days, Google is the number one underwriting tool for insurance companies other than classic in-person visitation. If you haven’t already, Google your building to see what an agent will see online, then take action to improve your property’s virtual presence. This might mean removing encampments, replacing a roof, and cleaning away graffiti.

Practice preventative maintenance. If you don’t have a regular and consistent maintenance plan in place, it could lead to higher rates. Keep in mind that many industrial buildings were constructed 40 years ago or more, which puts them at the tipping point when it comes to insurance. Carriers are looking very stringently at buildings that have not been well maintained, but making regular improvements can improve your odds of good coverage.

Commercial Property Insurance

Commercial property insurance covers the physical building of your business and all of its business assets including inventory, products, equipment, furniture, personal property). This commercial property insurance coverage provides protection for types of damage from fire, theft, natural disasters, and vandalism. It is necessary if you own or lease your property.

You can insure your property on a replacement cost or actual cash value basis. Replacement cost reimburses you the actual amount to replace the lost or damaged item. Actual cash value is the replacement cost minus depreciation—which may not be enough to replace the damaged property.

Commercial crime insurance and equipment breakdown coverage are insurance policies that can be grouped under commercial property coverage.

Casualty Insurance

Casualty insurance is a group of liability policies to protect your business from any liability claim you may face. It usually includes these types of commercial insurance coverage:

General liability insurance: General liability coverage protects your business from liability if a third party suffers bodily injury or any other accidents on your property. Damage to their property and advertising injury are also covered under this insurance policy.

Workers’ compensation insurance: Workers’ compensation insurance helps protect your employees from on-the-job injuries. If an employee is accidentally injured at work, it will cover their medical expenses and a portion of their lost wages.

Errors and omissions insurance: If you make a professional error in the course of your work, it can cause serious issues. A client may sue you for damages, which is where a professional liability policy can help protect you and your business.

Cyber liability insurance: Cyber liability protects your customer’s data. If it’s compromised, this insurance covers notifying your customers, credit monitoring, and identity theft protection.

Employment practices liability insurance (EPLI): EPLI protects a business if an owner or manager is accused by employees of sexual harassment, discrimination, wrongful termination, etc. It can help cover the cost of a legal defense and possible settlements.

Directors and officers liability insurance: D&O Insurance protects directors and officers and their personal assets from losses if they’re sued for actual OR alleged wrongful acts while they manage a company or organization. It covers legal fees and other costs associated with claims.

Commercial umbrella insurance: An umbrella policy helps you cover claims if they exceed the limits of an underlying policy. It can be more cost-effective to purchase this insurance instead of upping the limits of other policies.

Commercial auto insurance: Commercial auto protects your business and employees if accidents occur that damages another vehicle or property.

Commercial property and casualty insurance are often sold together as a package deal, similar to a business owners policy. We recommend speaking with an agent to determine what types of casualty coverage you need to include in your insurance package based on your business type.