Once you’ve opened escrow on a commercial real estate property, you will receive a preliminary report that describes the terms under which a title insurance policy will be issued for a specific parcel of land. It’s important to review this report so you understand any exceptions or exclusions from the title policy prior to completing your purchase.

WHAT IS A PRELIMINARY REPORT?

A preliminary report shows the ownership of a specific parcel of land, together with the liens and encumbrances tied to the property that will not be covered under a subsequent title insurance policy.

WHAT ROLE DOES A PRELIMINARY REPORT PLAY IN THE REAL ESTATE PROCESS?

While every property will have some exceptions, certain exceptions must be removed before a title policy can be issued. The preliminary report provides an opportunity for the parties to the real estate transaction and their agents to review and discuss items referenced in the report that are objectionable to the buyer prior to purchase.

WHEN AND HOW IS THE PRELIMINARY REPORT PRODUCED?

Shortly after escrow opens, the title company will begin assembling and reviewing certain recorded matters related to the property and the parties to the transaction. This may include things like a deed of trust recorded against the property or a lien recorded against the buyer or seller for an unpaid court award or unpaid taxes. These recorded matters are then listed numerically as “exceptions” in the preliminary report.

WHAT SHOULD I LOOK FOR WHEN READING MY PRELIMINARY REPORT?

You will be primarily interested in the extent of your ownership rights, so first review the ownership interest in the property you will be buying. The name of the owner of record shown in the report should match the name of the seller on your transaction. If the names don’t match, contact your escrow or title officer. You will also see the statement of vesting, which shows the form of the owner’s interest in the real property. “Fee” or “fee simple” is the highest type of ownership interest an owner can have. In some transactions, the interest might be a lease hold estate.

Next, you’ll see a reference to the legal description of the property, which is typically included in a separate schedule. There may also be a plat map or assessor’s map illustrating the location of the property. These maps are generated by the Los Angeles County Assessor for all property types including industrial real estate warehouses.

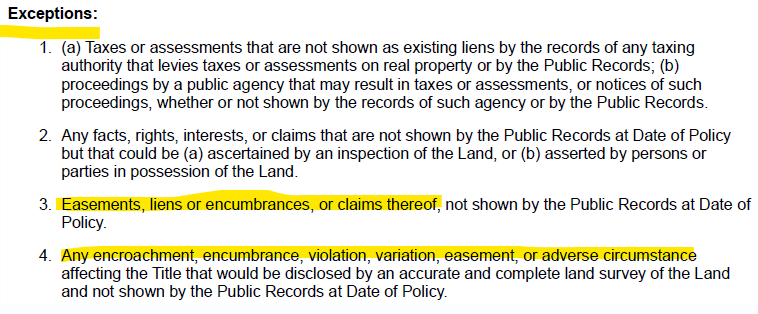

Finally, the report will reflect the exceptions, or those matters that will not be covered by the title insurance policy. Any transfer or encumbrance of this property will be subject to these exceptions unless steps are taken to eliminate them. Common exceptions include:

– Claims by creditors who have liens or liens for payment of taxes or assessments.

– Rules and regulations known as covenants, conditions and restrictions (CC&Rs) that must be followed by every homeowner in a covered community.

– Easements that give another party a right or interest in a property, such as providing a utility company access to install and maintain equipment or allowing a neighbor to cross over the property to gain access to their property.

– A deed of trust for any existing loan against the property.

Every title insurance policy will also contain an exhibit that lists exclusions from coverage. While the exceptions above are generally related to the subject property, exclusions are preprinted limitations on coverage that are included in all policies of the same type. It’s important to review this section, as it sets forth matters that will not be covered by your title insurance policy but that you may wish to investigate, such as governmental laws or regulations governing building and zoning.

If you have questions about the preliminary report, contact your title representative or escrow officer.

IS A PRELIMINARY REPORT THE SAME THING AS TITLE INSURANCE?

No. A preliminary report is simply a statement of terms and conditions of the offer to issue a title insurance policy; it is not a representation as to the condition of title. No contract or liability exists until the title insurance policy is issued.